Advancing Social Accountability Through Big Data, Ethics, and Environmental Research

Accounting is often perceived as a neutral tool for financial reporting, but research by Dean Neu and Gregory Saxton reveals its powerful role in shaping social accountability. Their work explores how accounting mechanisms, digital platforms, and professional ethics influence public discourse, corporate transparency, and environmental responsibility. By combining Big Data analytics, artificial intelligence, and qualitative methods, they examine how citizens, professionals, corporations, and regulators use accounting to demand accountability and drive social change. Both scholars bring unique expertise to this research domain.

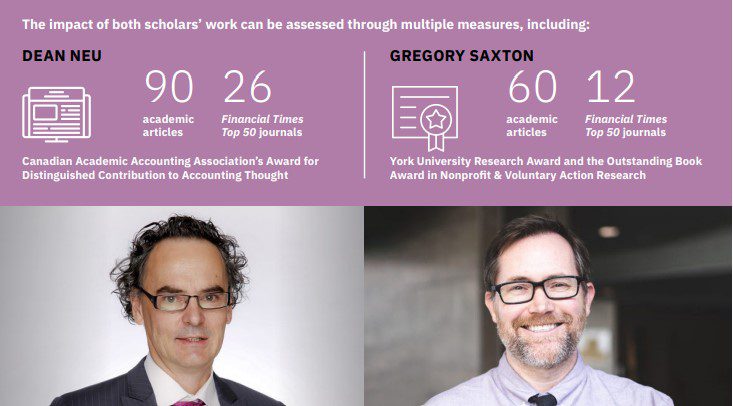

Dean Neu, Professor of Accounting, Schulich School of Business, York University, is an authority on public interest accounting and governance mechanisms. As the former co-editor of Critical Perspectives on Accounting, one of the field’s most influential journals, Neu has shaped public interest discourse in the discipline for over two decades. His research investigates how accounting is used to govern society and how marginalized communities respond to financial regulations. He has published over 90 academic articles, including 26 in pinnacle Financial Times 50 journals, and in 2016 was awarded the Canadian Academic Accounting Association’s highest honour – The Award for Distinguished Contribution to Accounting Thought.

Gregory Saxton, Professor of Accounting, Schulich School of Business, York University, specializes in data analytics, corporate social responsibility, and nonprofit accountability. His research applies machine learning and natural language processing to analyze social media discourse, financial disclosures, and governance mechanisms. A prolific scholar, Saxton has published over 60 peer-reviewed articles, including 12 in Financial Times Top 50 journals, and has received multiple accolades, including the York University Research Award and the Outstanding Book Award in Nonprofit & Voluntary Action Research.

Together, Saxton and Neu have pioneered a social accountability research agenda that examines the intersection of accounting, social movements, and public accountability. In many of their projects, they co-author with graduate students and Schulich Accounting Professors, Abu Rahaman and Jeffery Everett, further advancing research on financial accountability and governance.

Social Accountability in the Digital Age

Their first major research stream focuses on Twitter-Based Social Accountability – Investigating how Non-Governmental Organizations (NGOs), activists, and even bots use social media to hold corporations and governments accountable.

In an era of increasing digital activism, X (formerly known as Twitter) and other social media platforms have emerged as key tools for social accountability. Saxton and Neu’s research explores how NGOs, activists, journalists, and even bots use digital spaces to challenge corporate misconduct, expose unethical behaviour, and pressure organizations for transparency.

A central focus of their work is how accounting language—financial metrics, disclosures, and reporting standards—plays a role in online accountability movements. Their studies of #OccupyWallStreet, the Panama Papers, and corporate callouts analyze how social actors mobilize financial and ethical arguments to demand action from corporations and regulators.

“Our research consistently shows that numbers speak louder than words in social accountability movements,” notes Saxton. “When activists back their claims with financial data, their arguments gain significantly more traction with both the public and decision-makers.”

Their key findings reveal that financial inscriptions-based messaging (e.g., citing earnings reports, tax records, and financial misstatements) is more persuasive than values-based rhetoric in social accountability movements. Additionally, Twitter bots significantly influence corporate accountability discussions, amplifying or suppressing narratives to shape public perception. Perhaps most importantly, social media platforms serve as sites of deliberation, where activists and professionals use accounting discourse to “speak truth to power” and influence decision-makers.

Through Big Data analysis of millions of tweets, Saxton and Neu demonstrate that social media is not just a communication tool—it is an arena where accounting numbers become instruments of accountability and resistance.

Professional Ethics and the Accounting Profession

Their second stream of joint research concentrates on Professional Ethics in Accounting – Examining how ethical narratives evolve in the accounting profession and how financial experts justify or challenge unethical behaviour.

Ethical narratives play a crucial role in shaping public trust in the accounting profession. Saxton and Neu’s research explores how professional bodies, corporate leaders, and industry publications frame ethics to influence regulatory decisions, professional identity, and public perception.

A key focus of this work examines letters to the editor and editorial discourse in leading accounting journals, such as the Journal of Accountancy and CA Magazine. By analyzing these texts, they reveal how the profession justifies, debates, and evolves its ethical standards over time.

Their analysis identifies three critical patterns in professional ethics discourse:

- First, editorial narratives shape the profession’s ethical self-concept, often framing ethical concerns through a corporate rather than public-interest lens.

- Second, ethical dilemmas in accounting are often resolved through institutional experimentation, with professional bodies selectively adopting and discarding ethical standards based on economic and political pressures.

- Third, public engagement with ethics in accounting is episodic, with high-profile scandals driving bursts of discourse, followed by periods of institutional normalization.

Environmental Accountability and Corporate Transparency

Their third stream of co-authored research focuses on Environmental Accountability –and involves Big Data and AI to analyze corporate disclosures, assess greenwashing practices, and evaluate the impact of financial regulations on sustainability.

As environmental concerns grow, corporate sustainability reporting has become a critical tool for accountability. Saxton and Neu’s research investigates how accounting disclosures shape corporate environmental responsibility, particularly in the mining and energy sectors.

Through sophisticated textual analysis and machine learning techniques, they’ve developed metrics to assess not just the quantity but also the quality of environmental disclosures. Their research has identified concerning trends: The volume of environmental reporting has increased, but much of it is either repetitive disclosures that are carried forward year-by-year from previous reports or boilerplate language that buries critical information. Perhaps most importantly, they’ve demonstrated that regulatory changes in the Alberta energy sector can have significant real-world environmental consequences—highlighting the critical role of accounting research in evaluating and shaping policy outcomes.

The CPA Ontario Centre in Digital Financial Information

As Co-Directors of the CPA Ontario Centre in Digital Financial Information, Saxton and Neu are advancing research at the intersection of digital finance, accounting, and social accountability. Established through a strategic partnership between the Schulich School of Business and Chartered Professional Accountants of Ontario, the Centre serves as a vital hub connecting academic innovation with professional practice.

The Centre focuses on three core objectives:

- Building digital financial expertise among practitioners and students;

- Producing cutting-edge research on digital accounting information, and;

- Fostering collaboration between industry, academia, and regulatory bodies.

Through its workshop series, research forums, and executive education programs, the Centre addresses emerging challenges in digital financial reporting, data analytics, and AI-driven accounting processes.

“The accounting profession is undergoing a fundamental transformation driven by digitalization,” says Saxton. “Our Centre is uniquely positioned to help professionals navigate this change while ensuring that digital innovations enhance rather than compromise accountability.”

The Centre also plays a crucial role in translating academic research into practical insights for industry. Recent initiatives have included workshops on blockchain accounting, seminars on AI ethics in financial reporting, and research presentations on digital transparency mechanisms. By bridging theory and practice, the Centre helps ensure that accounting research has real-world impact.

Recent Research and Future Directions

Saxton and Neu’s research continues to evolve, integrating new technologies, regulatory developments, and social accountability trends. Their current projects represent perhaps their most ambitious and impactful work yet, addressing critical environmental accountability challenges in resource extraction industries.

One flagship project, “Inciting Environmental Accountability in Mining,” applies cutting-edge natural language processing to analyze Annual Information Forms filed by Canadian mining companies from 1998 to 2023. This comprehensive analysis of 152,567 environmental sentences reveals both promising and concerning trends in environmental disclosure practices.

“We’ve found that while companies are saying more about environmental issues, they aren’t necessarily saying anything more meaningful,” explains Neu. “The proportion of specific and novel environmental information has actually declined relative to boilerplate language, effectively burying useful information in a growing sea of generic statements.”

This research not only documents problematic disclosure practices but also demonstrates how advanced text analytics can generate actionable metrics to foster accountability. By developing tools to identify companies with consistently poor environmental reporting, Saxton and Neu aim to incite improved transparency and performance.

Their second major environmental project, “Accounting for the Environment: Regulation in Alberta’s Oilpatch,” examines how accounting-based regulatory mechanisms can drive environmental responsibility in the energy sector. This case study reveals the concrete environmental consequences of regulatory decisions, showing how the withdrawal of Alberta’s Long-Term Inactive Well Program in 2000 has resulted in significant ongoing environmental damage, including annual methane emissions equivalent to those from 75,000 gas-operated vehicles.

This research shows that accounting isn’t just about measuring environmental impact—it’s about creating regulatory frameworks that actually change corporate behaviour,” says Saxton. “When designed properly, accounting-based constraint mechanisms can capture the attention of industry participants and drive genuine environmental improvements.”

Through these cutting-edge projects, Saxton and Neu continue to demonstrate how accounting research can contribute to solving our most pressing social and environmental challenges. By combining methodological innovation with a commitment to social accountability, their work exemplifies how academic research can drive meaningful change in both professional practice and public policy.

Both Saxton and Neu noted the significance of Schulich’s community of world-leading researchers and colleagues in encouraging their research endeavours. They also noted the importance of the Schulich Research Office’s support in securing internal and external research grants. Beyond the research culture and events at Schulich, they both have benefitted greatly from the internal Schulich Research Excellence Fellowships. In addition, since 2000, Saxton and Neu, individually and in collaboration, have received over $400,000 (CAD) from federal funding agencies (SSHRC) and CPA Ontario to support their research program.